This acrylic and oil painting is on a 24×36 canvas.

Title: Inner Peace

This acrylic and oil painting is on a 24×36 canvas.

Title: Inner Peace

As subscribers and daily readers of the Wall Street Journal (print and online) we found the following article extremely telling in light of our past success and current work focus:

Chinese Cash Pours into U.S. Real Estate

Site on San Francisco Bay reflects a move into new development, beyond buying existing commercial properties

Chinese developers are planning a $1 billion commercial project on this San Francisco Bay property. Photo: Greenland USA

By Eliot Brown – Aug. 30, 2016 11:02 a.m. ET

For eight years, a pair of local developers gradually readied a 42-acre strip of waterfront land 10 miles south of downtown San Francisco for a major project, steering it through local land-use approvals.

Now, a group of major Chinese developers is poised to do the heavy lifting. The venture of Greenland Holding Group, Ping An Trust and other investors paid $171 million last month for the site that juts into San Francisco Bay.

The new owners are planning a more than $1 billion development aimed at biotechnology companies, an industry flourishing in the area. “We are pretty confident about the local market and particularly about the research-and-development market,” said Taotao Song, chief executive of the venture.

Over the past three years, Chinese investors have plowed money into some of the highest-profile developments in the U.S. Other cities with projects underway or in the pipeline include New York, Boston, Chicago, Los Angeles and Miami.

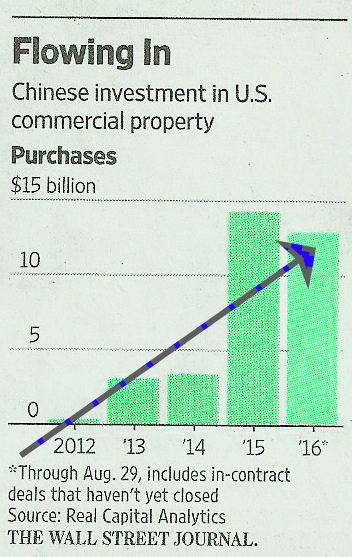

The flow of cash from China into U.S. commercial property is continuing unabated as companies seek to diversify outside of China at a time when confidence is fading in their local real-estate markets, real-estate executives say.

President Xi Jinping’s anti-corruption campaign has also compelled Chinese investors to seek projects abroad as a way to hedge against a possible crackdown to their business at home. Officials have blocked property sales and detained companies’ executives during investigations.

In the first half of 2016, completed U.S. commercial property purchases by China-based investors were up 19% over a year earlier to $5 billion, according to data tracker Real Capital Analytics Inc. Including deals under contract that haven’t been finished, Chinese investors have committed $12.9 billion this year, nearly matching the $14 billion in all of 2015. The rate of increase does appear to be slower this year, given that in 2014 there was just $3.4 billion in sales to Chinese investors, according to Real Capital.

Investments include office towers such as Manhattan’s 1285 Avenue of the Americas—in which China Life LFC -2.02 % Insurance Co. bought a partial stake—and Anbang Insurance Group Co.’s $6.5 billion deal to buy Strategic Hotels & Resorts Inc., which hasn’t closed. Anbang also led an aborted $14 billion purchase of Starwood Hotels & Resorts Worldwide Inc. HOT -0.37 %

Still, there are some headwinds back home for Chinese investors as officials seek ways to stanch the flow of money out of China. For those real-estate investors that do get money out, developing new buildings is a main focus, given that it offers far higher returns but also more risk than buying existing buildings.

“The vast majority are looking for development opportunities,” said Stephen Collins, who oversees a global capital markets group at real-estate investment-services company JLL. The Chinese companies have experience with development at home, and believe they “can make more money buying the land, building it and selling it,” than just buying an existing tower, he said.

Projects controlled or partly owned by Chinese companies include a development to create Chicago’s third-tallest tower; a planned tower that would be San Francisco’s second-tallest building; a cluster of giant mixed-use projects in downtown Los Angeles; and a planned skyscraper in downtown Boston by Chinese developer Gemdale Corp. 600383 3.62 %

Earlier this month, in one of the flashiest investments yet, China’s Shanghai Municipal Investment said it was joining with New York-based Extell Development Co. to build the $3 billion Central Park Tower. The condo skyscraper is set to rise 300 feet taller than the Empire State Building to become the tallest apartment tower in the U.S.

A rendering of Greenland Group’s $1 billion Metropolis development in Los Angeles. Photo: Greenland USA

For all of these projects, a big risk is timing. The U.S. is seven years into an economic growth cycle, making many wonder how much longer the good times can last. Much of this concern is focused on Manhattan’s luxury-condo market, where Chinese companies have funded a large crop of towers that are just being built, despite a slowdown in sales and widespread concerns about a condo glut.

The largest Chinese developer in the U.S. is Greenland Group, which has a $1 billion cluster of towers named Metropolis being built in Los Angeles. The company also owns 70% of a $6 billion apartment development in the New York borough of Brooklyn, where three towers have sprouted since it first invested in 2014. More are on the way.

Greenland executives predicted in mid-2014 that they would double their pipeline within a year and have considered numerous sites throughout the country. But the company ended up being less active than expected: its first U.S. deal since mid-2014 was the San Francisco Bay site it purchased for the biotech center.

The seller of that site was a venture of Shorenstein Properties and SKS Partners, which bought it in July 2008 for $85 million and won city approval for a 2.3 million-square-foot development.

Greenland and its partners plan to start moving ahead on a 500,000-square-foot first phase as soon as infrastructure work being done by the city of South San Francisco is completed in mid-2018. Greenland said the venture would begin construction whether or not any of the space is leased beforehand.

—Esther Fung contributed to this article.

Original Source: http://www.wsj.com/articles/chinese-cash-pours-into-u-s-real-estate-1472569340

By Daniel Goldstein, Personal Finance reporter for MarketWatch.com — Published: July 2, 2016 10:53 a.m. ET

Despite Brexit upheaval and stock market losses, U.S. real estate market appears on much more solid footing in 2016

When it comes to investing in the stock market, you may lose your shirt, but you probably won’t lose your home. In fact, when the equity market gets rough, real estate tends to be a life raft for investors seeking safety.

“Real estate is Americans’ preferred investment for money that they won’t need for at least 10 years and that hasn’t changed,” said Greg McBride, chief financial analyst with New York-based Bankrate.com. “Nervous investors always look to real estate rather than shy away from it in times of volatility.”

While global uncertainty spreads and stocks fall worldwide in the aftermath of the British referendum to leave the European Union, it doesn’t necessarily mean déjà vu all over again, at least when it comes to a repeat of the real estate plunge of 2007. The crash that began that year accelerated sharply following the 2008 rout of the equities market, when home prices in late 2011 were down more than 20% from their peak in spring of 2007.

“There is a lot of Brexit panic going on,” said Francis Greenburger, chief executive of Time Equities Inc., a real estate development firm in New York. “When you realize that this is going to play out over years, and nothing substantive is going to change in the short-term, it seems like an overreaction,” he said.

As a result, here’s why you shouldn’t be panicking post-Brexit if you’re looking to buy or sell a home:

Interest rates should stay low, and could go even lower.

And as markets reel post-Brexit vote, the pace of further Federal Reserve rate increases is likely to slow further, according to Kevin Finkel, senior vice president of Resource America Inc. REXI, -0.10% , a real-estate investment trust in Philadelphia.

“If the Fed had a decision to make to raise interest rates, it gets pushed back further now,” he said. “The slower growth in Europe that Brexit will likely cause and the worldwide global slowdown as a result will force the Feds to drag their feet.”

The Fed was already considering holding off on a summer rate increase when the news was announced earlier this month that the U.S. created just 38,000 new jobs in May and nearly half a million people dropped out of the labor force, raising doubts about the strength of the economy.

“The chances are the Fed is reading the (Brexit) signs as being negative to growth and activity,” said Time Equities’ Greenburger. “As long as inflation remains in check, the Fed is going keep their powder dry and leave rates as they are,” he said.

The 10-year Treasury, which mortgage rates follow, fell as much as 20 basis points since the results of the Brexit vote were announced. For someone in the market for a $200,000 home, the pre-vote rate of 3.46% would have cost $715 for a 30-year fixed-rate mortgage with a 20% down payment, according to Zillow’s mortgage group. A 20 basis point drop would make that monthly cost $697.

Finkel also notes that the uncertainty in Europe will mean the U.S. will continue to be a haven for real estate investors, pushing prices higher. Indeed, a survey of 700 Chinese real estate investors by the firm East-West Property Advisors Ltd. shortly after the Brexit vote results were announced, showed that 41% of those polled indicated they’d be more willing to invest in the U.S. residential market rather than in the U.K. “Chinese buyers are increasingly interested in the American real estate market because of the perceived safety that places such as New York and San Francisco, now offer compared to London,” the survey showed.

That could help millions of Americans who were unable to refinance because their homes were underwater (meaning they owed more on the home than it was worth). Research firm Black Knight estimates that as many as 7.4 million borrowers could refinance their homes and Brexit could mean even lower interest rates when they do so.

Moreover, as interest rates stay low, the impact of “rate-shock” when short-term adjustable rate mortgages (ARMs) readjust will be minor compared with what happened between 2007 and 2012, when many Americans could no longer afford their new housing payments and defaulted.

One downside to the low interest rates however is that private buyers of mortgage pools, the so-called mortgage-backed securities, are staying away from the market because rates of return are so low. That hurts liquidity and prevents banks from making more loans. As a result, government-sponsored enterprises have to buy up the majority of the loans to create liquidity in the market. According to the Housing Finance Policy Center of the Urban Institute in Washington, D.C., the private label securitization market was valued at $718 billion in 2007 and plunged to just $59 billion in 2008. It was valued at just above $64 billion in 2015.

There’s less risk of a new mortgage bubble

The percentage of loans in foreclosure nationally is the lowest level since April of 2007, according to Black Knight. Foreclosures reached a peak of 4.6% in 2011 at the height of the real estate bust. This year, just 575,000 homes were in active foreclosure in May, down from 800,000 a year ago, a 29% drop, according to Black Knight. While new foreclosures starts last month of 62,100 were up slightly from a 10-year low set in April, they are still 20% lower than a year ago, Black Knight said.

“The recent rise in bank repossessions represents banks flushing out old distress rather than new distress being pushed into the pipeline,” said Daren Blomquist, vice president of Irvine, Calif.- based RealtyTrac, a real-estate research company.

Unlike the 2005 to 2012 mortgage meltdown, when so-called liar loans and exploding ARM’s flooded the market, the subsequent pullback in credit may have been overly tight, but it does mean in 2016 there are fewer real estate bubbles waiting to pop. While it’s true there are markets that have seen incredibly inflated real-estate values such as San Francisco and New York, it’s not fueled by unsustainable and loose credit standards.

“The changes that have taken place over the past five to seven years have built a more stable foundation” in the mortgage industry, said Michael McPartland, a managing director and head of residential real estate for North America at Citigroup’s private bank. “There just aren’t a lot of the exotic products like interest-only [loans] and super-high loan-to-value [mortgages],” he said. “If things slow down, there will be a contraction, but not a pop.”

McPartland says with slow wage growth and high student loan burdens it may be harder for younger borrowers to afford a 20% down payment and monthly interest payments that are principal and interest, instead of just interest-only, but the flip side is increased home equity, so home buyers are less likely to leave the keys on the counter and walk away if things go bad.

Help for first-time home buyers

In 2014, the Federal Housing Administration began reducing mortgage insurance premiums on loans by an average of $900 a year, in an effort to nudge first-time home buyers and millennial borrowers who might not have much cash for a down payment to finally enter the housing market.

Those other federal moves include Fannie Mae and Freddie Mac making lower down payment loan options available to more borrowers. In 2014, the agencies began to buy loans with just a 3% down payment, or 97% loan-to-value ratio. Fannie Mae also announced in 2015 that it would allow income from a non-borrower household members to be considered as part of a loan applicant’s debt-to-income ratio. That could help some borrowers, who might have family members on Social Security or disability living with them, or a renter in a basement apartment, to boost their income levels and help them qualify for a loan.

Lower oil prices

At the end of 2008, gasoline prices, which had risen to a record $4 a gallon nationwide that summer, had crashed to under $2 a gallon. In that case, the cheap gas (and diesel) wasn’t a good thing, as the worldwide economy was shuddering to a halt.

While the U.S. economy (and world economy) is slowing down, the lowest gas prices since 2009, with the national average now close to $2 a gallon is likely to help the housing market.

“The continuing drop in gas prices is freeing up valuable disposable income,” says Resource America’s Finkel, which can help Americans absorb higher rent payments, or move up to a more expensive property.

Job growth

While jobs typically are a lagging indicator of an economic downturn, the U.S. has had a slow- but- steady rate of job creation for the past five years, though that appears to be tailing off in recent months. The U.S. had been averaging more than 200,000 new jobs a month since 2014 until a recent slowdown since March that’s seen hiring taper off to a 116,000 monthly range.

“The recession risks are elevated, but there’s not an abundance of people seeing one over the hood of the car,” said Mark Hamrick, senior economic analyst at Bankrate.com. Hamrick expects GDP growth to rebound in the second quarter at 2% for the rest of the year, which he said will be enough to support expansion in the housing market.

“I don’t think anybody is looking at the payroll numbers and deciding it’s a bad time to buy a home,” he said.

(With additional reporting by Andrea Riquier, Greg Robb and Jeffry Bartash)

Original Source Here: http://www.marketwatch.com/story/5-reasons-a-2009-style-real-estate-meltdown-is-unlikely-now-2015-08-25?link=afterbell

As producers of a variety of garden edibles, the importance of timely bee pollination is obvious. Around the world, the implications of decreasing food supplies due to declining bee colonies is a critical problem facing the future of our planet.

The most common cause for the bee decline is the use of pesticides. From around 6 million bee colonies in 1945, it is estimated that only 3 million bee colonies remained just 10 years ago.

Today, we had the great fortune of meeting a man on the move, dedicated to working with like-minded people to create a solution to the loss of pollinating bee populations. Dave Hunter, the founder and owner of Crown Bees, is rapidly growing a business supplying a species of bee (the Mason Bee) to offset the decline in Honey Bees, which has served as the main food pollinators in the past. The Mason Bee actually has superior pollinating characteristics, and is a gentle and easy to breed species.

We have begun creating a central place for Dave’s Crown Bees in our garden sanctuary, and have gained immediate enthusiasm for the species.

We have at the same time gained a great level of respect for Dave and the mission of the Crown Bee group he is forming to make a significant impact for ethical change on our planet.

Take a look at the CrownBee.com website and learn more about Mason Bees and how you can help change the course of history for the better.

Below is a quote from the CrownBee.com blog:

Science proved in the 1980’s that when mason bees were used in orchards, farmers increase the yield of their crop. Cherries can increase by 200-300 percent, almonds by less. Studies have been replicated in the US, Europe, and Asia for increased production of apples, pears, kiwi, peaches, and many other fruits and nuts which show amazing results.

These gentle mason bees exist in backyards and meadows worldwide. You might have them at your home, but until today, they have gone unnoticed. Gardeners are now using mason bees to gain more fruits and summer vegetables.

You can discover more about this astounding bee through reading the “learn” portion of Crown Bees website. You can raise this gentle bee yourself. Get started today.

This painting, “Benefaction” is in acrylic on a 30″ x 48″ wood panel. Frank portrays the challenge of a foggy day for a typical ship in trying to find its way along a rocky and dangerous coast.

It was a very joyful moment to see the light on the shore, while receiving guidance from a friendly sea-bird bringing the ship to the light. This allowed the ship to turn just in time to miss the hidden rocks and certain catastrophe.

May we all show compassion and do what we can to aid others avoid possible disasters that can appear so quickly for any of us.

In this first sketch of Frank’s lighthouse series, he was looking to illustrate different points of view around the initial intended function of lighthouses over 100 years ago.

In this 28” x 18” pastel on illustration board, Frank wonders what it would be like for a sailor at sea for months. Would he dream about seeing a light? Would he trust his eyes or think it a vision when finally seeing a light?

This week, we will explore some of Frank’s lighthouse art and share meanings we can reflect on today. Thank you for stopping by!